Market Overview:

-

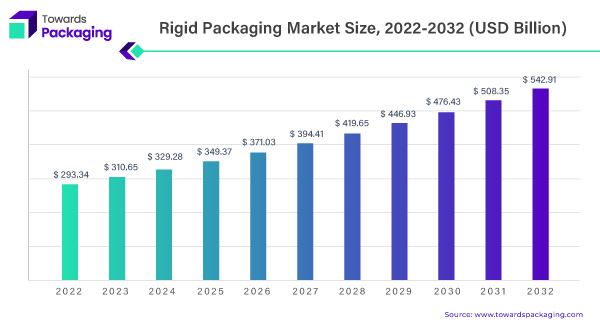

- Rigid plastic packaging market size valued at USD 310.65 billion in 2023.

- Anticipated to reach USD 542.91 billion by 2032.

- Projected CAGR of 6.4% from 2023 to 2032.

Industry Applications:

-

- Widely used in pharmaceuticals, food and beverages, electronics, personal care, etc.

- Food and beverage industry major consumer, driven by the demand for convenient food products.

Industry Drivers:

-

- Global growth in various sectors (food and beverage, healthcare, personal care).

- Attributes: durability, lightweight construction, versatile packaging.

- Manufacturing processes: extrusion, injection molding, blow molding, thermoforming.

Cosmetics and Personal Care Sector:

-

- Significant use in sun care, skin care, oral care, perfume, body care, and hair care.

- Growing demand in tandem with the expanding cosmetics and personal care industry.

- Emerging economies like Malaysia and Thailand show substantial growth projections.

Cosmetics and Personal Care Industry Factors:

-

- Consumer base growth, changing lifestyles, and increased disposable income.

- Demand for high-quality packaging due to increased personal grooming awareness.

- Rigid plastic packaging meets requirements effectively with versatility, durability, and aesthetic appeal.

Market Expansion Strategies:

-

- Manufacturers investing in advanced technologies, innovative designs, and sustainability.

- Focus on recyclable and biodegradable materials to align with environmental responsibility.

- Meeting regulatory considerations emphasizing sustainability in packaging.

Regional Perspective:

-

- Asia Pacific dominates the market, with China and India driving growth.

- Growing economies and increased economic activity contribute to market expansion.

- Latin America experiences promising growth rates, prioritizing convenience and practicality over environmental concerns due to challenges like economic or political instability and ongoing pandemic repercussions.

Rigid Plastic Packaging Market: Segment Analysis and Growth Prospects

The rigid plastic packaging market’s leading segment in market value and market share has emerged as the bottles and jars category. Additionally, it is anticipated to have the second-highest Compound Annual Growth Rate (CAGR) throughout the forecast. According to the LAMEA region, the expected CAGR for this category is 3.3%. Water, cosmetics, carbonated soft drinks, food, juice, personal care products, and pharmaceuticals are all packaged using rigid plastic bottles. PET, PP, PS, PE, HDPE, and PVC are the main materials used to make these bottles and jars.

Instance, May 2023, LanzaTech and Plastipak Partner to Produce World’s First PET Resin Made from Waste Carbon

This market is expanding due to the growing retail industry and rising consumer disposable income. The market is further stimulated by the rising demand for beverages and home care products, ongoing urbanization, and population growth.

, By Types & By End-user, By Country, 2022-2030")

The food and beverage sector emerged as the dominant market for rigid plastic packaging in 2023, with significant growth anticipated in the South African region, projected at a Compound Annual Growth Rate (CAGR) of 4.1% from 2022 to 2030. Rigid plastic packaging offers numerous advantages to containers, including taste preservation, durability, extended lifespan, and lightweight properties. Bottles, cans, jars, and other forms of rigid plastic packaging containers ensure the security and protection of food items, preventing contamination

The demand for rigid plastic packaging is rapidly increasing in developing countries such as the United States, Canada, China, India, and other nations, primarily driven by the expanding food and beverage sector. As the food and beverage industry grows, the demand for rigid plastic packaging will rise accordingly.

Capitalizing on the Surge: Exploring Opportunities in the Booming Healthcare Sector

In response to the global pandemic, governments worldwide are implementing extensive investments in healthcare infrastructure development within developing nations. These strategic initiatives aim to enhance these regions’ healthcare capabilities and facilities. Notably, rigid plastic packaging has emerged as a vital component in ensuring the safety and integrity of medical supplies, such as pharmaceuticals, needles, tablets, syrups, surgical equipment, and other essential items. The inherent qualities of rigid plastic packaging, including its strength, cleanliness, clarity, and lightweight nature, make it an ideal choice for securely storing these medical products.

The escalating growth of the healthcare sector on a global scale is anticipated to significantly contribute to the rising demand for rigid plastic packaging. Projections based on the staff research report of the “US-China Economic and Security Review Commission” indicate that the Chinese healthcare market alone is expected to reach a staggering 16 trillion RMB (equivalent to approximately US$ 2.3 million) by 2030. These estimations further support the notion that the expansion of the healthcare industry will serve as a driving force behind the growth of the rigid plastic packaging market.

Therefore, during the forecast period, it is anticipated that the increasing prominence of the healthcare sector will fuel the expansion and market opportunities for rigid plastic packaging. This emerging trend opens avenues for businesses operating in this sector to capitalize on the growing demand. Companies involved in the production, supply, and distribution of rigid plastic packaging are poised to benefit from this anticipated surge in market growth.

To fully leverage this opportunity, businesses need to align their strategies with the evolving needs of the healthcare sector. This includes investing in research and development to create innovative and specialized packaging solutions that cater to the specific requirements of the medical industry. Moreover, companies should focus on establishing strong partnerships and collaborations with healthcare organizations, government bodies, and regulatory authorities to ensure compliance with industry standards and regulations.

Furthermore, businesses should prioritize sustainability and environmental consciousness in their packaging practices. Like many others, the healthcare industry is increasingly concerned with minimizing its ecological footprint. Therefore, implementing eco-friendly packaging solutions, such as recyclable and biodegradable materials, can provide a competitive advantage while addressing the industry’s sustainability goals.

In conclusion, the ongoing investments by governments in healthcare infrastructure development, combined with the projected growth of the healthcare sector, create a favourable business environment for the rigid plastic packaging market. Companies that proactively adapt their strategies to meet the demands of this expanding market while prioritizing sustainability are well-positioned to capitalize on emerging opportunities and achieve long-term success in this dynamic industry.

Fuelling Expansion: Surging Demand from the Food and Beverage Packaging Market

The rigid plastic packaging market is experiencing a surge in demand across various end-use industries, including food and beverages, cosmetics and toiletries, and healthcare. Among these industries, the food and beverage sector has consistently held the highest share in the overall packaging industry. The growth in this sector has significantly impacted the packaging market as a whole.

In particular, the retail industry is undergoing a notable transformation from unorganized to organized retail, which is expected to further drive the demand for rigid plastics as packaging materials. This shift in the retail landscape is likely to create new opportunities and stimulate the growth of the rigid plastic packaging market.

The beverage sector emerges as a major consumer of rigid plastic packaging within the food and beverage industry. This is primarily due to the ability of rigid plastic packaging to preserve the quality and freshness of the products by effectively sealing the contents within the container. Several factors contribute to the increased consumption of rigid plastic packaging in the beverage industry.

Firstly, the rise in disposable income among consumers has led to changes in their lifestyles and purchasing habits. As a result, there is a growing demand for convenient and packaged beverage products that can be easily consumed on the go. Rigid plastic packaging provides a suitable solution, offering convenience and portability.

Secondly, product presentation and differentiation are crucial in the beverage industry. Rigid plastic packaging allows for attractive and eye-catching designs, enhancing the visual appeal of the products on store shelves. This visual appeal plays a vital role in capturing customer attention and influencing purchasing decisions.

Furthermore, the increasing demand for specific beverage products, such as packed bottled water and alcoholic beverages, is expected to contribute to the consumption of rigid plastic packaging. These products often require sturdy and reliable packaging solutions to ensure product safety and prevent leakage or contamination.

In conclusion, the demand is driven by various factors, including the growth of end-use companies such as healthcare and cosmetics, food and beverages, and toiletries. Within these industries, the food and beverage sector hold a significant share, with beverage manufacturing being a crucial customer of rigid plastic packaging. The rise in disposable income, product presentation, differentiation, changing customer lifestyles, and the demand for specific beverage products all contribute to the increased utilization of rigid plastic packaging. As the market continues to evolve, businesses operating in the rigid plastic packaging sector should align their strategies to meet the growing demands of these industries and capitalize on emerging opportunities.

Comparative landscape

In the competitive landscape of the rigid plastic packaging industry, companies are constantly striving to differentiate themselves and gain a competitive edge. Rigid plastic packaging has emerged as a popular choice across various sectors due to its durability, versatility, and cost-effectiveness.

To succeed in this comparative landscape, businesses must focus on crucial factors such as sustainability, technological advancements, and meeting shifting consumer preferences. Sustainability has become a critical consideration with the increasing demand for environmentally friendly packaging solutions. Companies invest in research and development to create sustainable alternatives like biodegradable or recyclable materials. Technological advancements also play a crucial role, enabling the development of innovative manufacturing processes, materials, and smart packaging solutions.

Staying at the forefront of these advancements allows companies to offer cutting-edge packaging solutions that meet the evolving needs of their customers. Moreover, businesses must closely monitor market trends and consumer preferences to adapt their offerings accordingly. This includes addressing convenience, aesthetics, and eco-consciousness in packaging design. Streamlining supply chains and optimizing costs are essential to remain competitive in rigid plastic packaging. By embracing sustainability, technological innovation, and customer centric strategies, companies can position themselves for success in this competitive landscape.

Major key players in rigid plastic packaging market are ALPLA-Werke Alwin Lehner GmbH & Co KG, Amcor Limited, DS Smith Plc, Berry Plastics Corporation, Klöckner Pentaplast, Plastipak Holdings, Inc., Pactiv Evergreen Inc, Sealed Air Corporation, Silgan Holdings, Inc., Sonoco Products Company.

Segments covered in the rigid plastic packaging market

By Type

- Bottles & Jars

- Rigid Bulk Products

- Trays

- Tubs, Cups, & Pots

- Others

By Production Process

- Extrusion

- Injection Molding

- Blow Molding

- Thermoforming

- Others

By Material

- Polyethylene (PE)

- Polyethylene Terephthalate (PET)

- Polystyrene (PS)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Expanded Polystyrene (EPS)

- Bioplastics

- Others (PC, Polyamide)

By End User

- Food

- Meat, Seafood, and Poultry

- Ready to Eat Meals

- Dairy Products

- Bakery and Confectionery

- Other Food Products

- Beverages

- Alcoholic Beverages

- Non-alcoholic Beverages

- Healthcare

- Cosmetics & Toiletries

- Industrial

- Others

By Geography

-

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa (MEA)